Your commercial asset isn't just a physical structure; it's a strategic financial instrument wrapped in concrete and glass. If you're asking how to value my commercial property in the current Melbourne market, you've likely discovered that the old rules of thumb no longer apply. With the Reserve Bank of Australia setting the cash rate at 4.35% in May 2026, the gap between a standard bank valuation and a true market appraisal has never been wider or more critical to your bottom line.

It's natural to feel a sense of confusion when calculating net income versus gross income, or to worry about how shifting interest rates are compressing yields across the South East. We understand that elite investors in the City of Casey require precision rather than guesswork to make informed portfolio decisions. This guide promises to demystify the sophisticated Cap Rate method and provide you with the exact framework professional valuers use to determine an asset's true market worth.

We'll provide a definitive checklist of documents you need for a successful valuation and share proven strategies to increase your property's value before you even speak to an agent. You'll also gain insights into current industrial yields, which remain a standout in the South East at 5.25% to 6.00%, ensuring you have the localized knowledge to stay ahead of the curve.

Key Takeaways

- Learn the technical differences between Income Capitalisation and Direct Comparison to identify the most accurate valuation strategy for your specific asset.

- Discover exactly how to value my commercial property by analysing how the WALE factor and tenant strength directly influence your market yield.

- Master the documentation process required to present a transparent and high-performing investment case to professional valuers.

- Leverage specialised insights into the shifting industrial and retail yields across Berwick and Narre Warren to stay ahead of South East market trends.

- Uncover practical methods to enhance your property’s physical appeal and income potential before undergoing a professional appraisal.

What is Commercial Property Valuation?

Commercial property valuation is the rigorous process of calculating an asset's market price by weighing its income potential against inherent risks. Unlike residential assessments, which often rely on emotional appeal or nearby sales of similar houses, a Real estate appraisal for a commercial asset focuses on the cold, hard data of lease agreements and yield expectations. In Australia, the Australian Property Institute (API) sets the professional standards that certified valuers must follow to ensure accuracy and ethical transparency.

When you're trying to understand how to value my commercial property, it's vital to distinguish between a formal valuation and a market appraisal. With the Reserve Bank of Australia holding the official cash rate at 4.35% as of May 2026, the financial environment for investors is increasingly nuanced. You'll typically need a formal, fee-based valuation for bank financing, legal disputes, or superannuation auditing. Conversely, a market appraisal is a strategic tool used when you're preparing for commercial leasing and management or considering selling. This appraisal provides a real-time snapshot of what tenants or buyers in the City of Casey are currently willing to pay.

The Core Difference: Income vs. Capital Growth

Commercial assets operate more like businesses than passive shelters. While residential investors often chase capital growth through land appreciation, commercial investors prioritise the cash flow generated within the building's walls. This shift in focus moves the priority from total land size to Net Lettable Area (NLA). NLA represents the actual space a tenant can occupy and pay rent on, excluding common areas like foyers or lift wells.

A vacant commercial building often carries a lower value than an identical tenanted one. This is because a vacancy represents an immediate risk and a lack of proven income. A secure lease with a reputable tenant transforms a physical structure into a reliable financial product, which is exactly what sophisticated Melbourne investors are looking to acquire.

Key Terminology to Organise Your Strategy

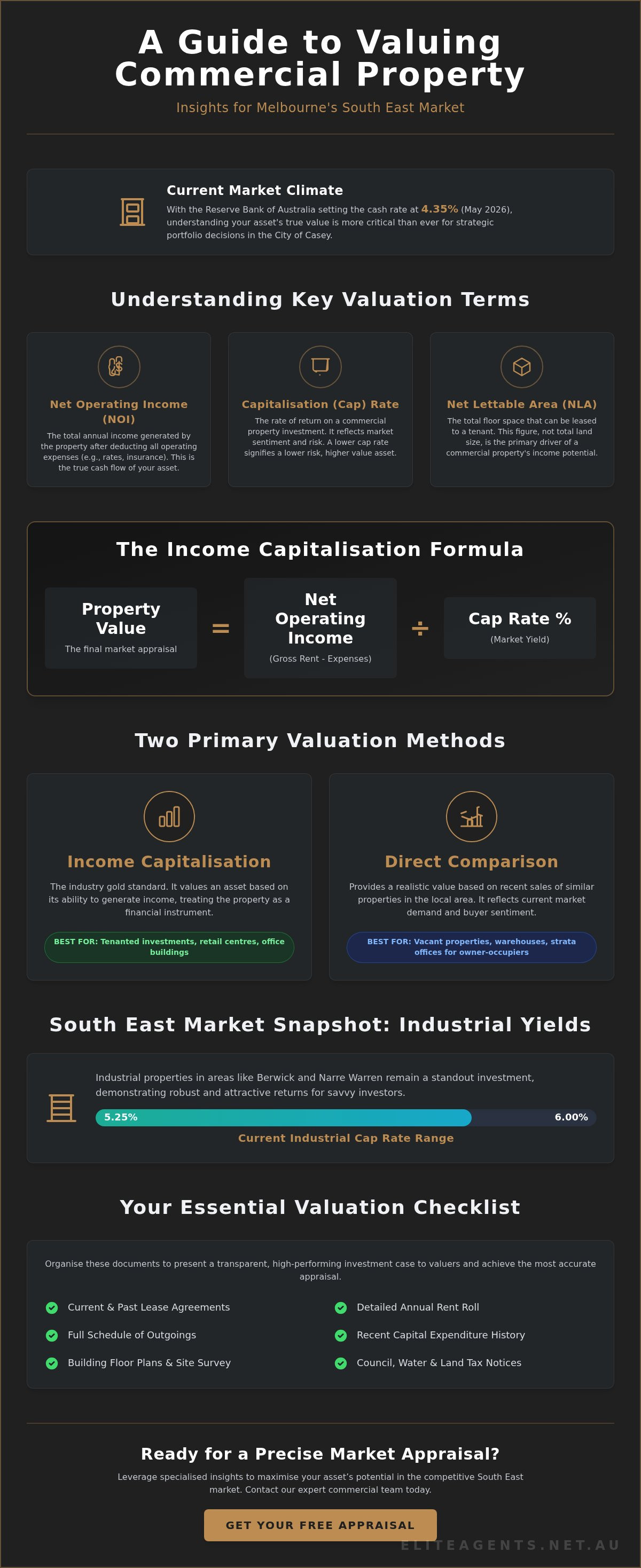

To master the valuation process, you must first understand Net Operating Income (NOI). This is the foundation of your asset's value; it's the total annual income minus all operating expenses. Unlike residential properties where the landlord often absorbs many costs, commercial leases frequently require the tenant to pay for outgoings. These include council rates, building insurance, and land tax. Under Victorian legislation for contracts entered into in 2026, remember that land tax costs cannot be passed to the buyer for properties sold below the $10.7 million threshold.

The final piece of the puzzle is the Capitalisation (Cap) Rate. In the Melbourne market, the Cap Rate reflects the expected rate of return on an investment. A lower Cap Rate usually indicates a premium, low-risk asset in a high-demand area like Berwick, while a higher rate suggests greater risk or a secondary location. Understanding these metrics allows you to view your property through the same lens as a professional valuer.

The Two Primary Methods: Income Capitalisation vs Direct Comparison

When you're investigating how to value my commercial property, you'll encounter two dominant schools of thought. The Income Capitalisation method is widely considered the industry gold standard for tenanted investments because it treats the property as a financial yield-producing vehicle. However, for warehouses and office suites destined for owner-occupiers, the Direct Comparison method often provides a more realistic reflection of local demand. Occasionally, valuers use the Summation Method, which assesses land and improvements separately; this is usually reserved for specialised assets or insurance purposes. In the competitive South East Melbourne market, we often employ a hybrid approach to ensure your asset is positioned with absolute precision.

Mastering the Cap Rate Formula

To accurately determine the value of your property, you must first calculate your Net Operating Income (NOI). Start with your gross annual rent and subtract all non-recoverable outgoings. Once you have this figure, you apply the market Capitalisation (Cap) Rate. As of May 2026, industrial assets in the South East typically command yields between 5.25% and 6.00%, while neighbourhood retail sits between 5.00% and 6.50%.

Consider this example: if your warehouse in Berwick generates a net income of A$100,000 per annum and the local market yield is 6%, your property value is approximately A$1.66 million. Small shifts in this percentage can significantly impact your equity, which is why understanding localised data is non-negotiable. If you're unsure where your asset sits on this spectrum, a free commercial property appraisal can provide the clarity you need to move forward with confidence.

When Direct Comparison Takes Priority

There are times when the income isn't the primary driver of value. If you're selling a vacant warehouse in Pakenham or an office suite in Officer, the buyer is likely a business owner looking for a permanent home rather than an investor seeking a yield. In these cases, we look at the rate per square metre ($/sqm) achieved by recently sold, similar properties.

This method requires a sharp eye for detail. We don't just look at the floor area; we adjust for building age, internal clearance height, and the number of roller doors. A modern facility with high-clearance racking and wide-turning circles for heavy vehicles will always command a premium over older, more restrictive stock. By comparing these physical attributes against current market transactions, we establish a value that reflects the tangible utility of the space for a working business. This approach ensures you don't leave money on the table when dealing with owner-occupier buyers who value function over financial statements.

Beyond the Numbers: Factors That Swing Commercial Value

While the mathematical precision of yields provides a baseline, the true worth of your asset often lies in the fine print of your lease agreements. Sophisticated investors understand that a building's physical shell is only half the story; the other half is the quality of the income it produces. When you are assessing how to value my commercial property, you must look past the bricks and mortar to evaluate the strength of your tenant and the structure of their commitment. A "national brand" tenant provides a superior tenant covenant, acting as a financial shield that reduces perceived risk and allows for a more aggressive Capitalisation Rate.

Lease structures also play a pivotal role in your final valuation. Net leases, where the tenant covers outgoings like insurance and council rates, are generally preferred by investors seeking predictable cash flow. However, you must stay informed about evolving Victorian regulations. For contracts entered into in 2026, remember that land tax costs cannot be passed on to buyers for properties priced below the $10.7 million threshold. These legislative shifts directly impact your property's "clean" net income and, consequently, its market value. For those seeking to align their assets with professional standards, the Australian Valuers Institute provides the ethical and professional framework that underpins high-level appraisals in Melbourne.

The Power of a Secure Lease

A five-year lease with multiple options for renewal is exponentially more valuable than a month-to-month arrangement. Stability is a currency in commercial real estate. You should also scrutinise your rent review mechanisms; fixed percentage increases or CPI-linked reviews ensure your income keeps pace with the 4.6% annual inflation rate recorded in March 2026. WALE represents the remaining life of your income stream; it's the primary metric professional investors use to quantify vacancy risk. A long WALE suggests a "set and forget" investment, which commands a premium price in the City of Casey.

Physical Attributes and Future Potential

Zoning dictates your property's ceiling. A "Commercial 1" zone offers different development upside compared to "Industrial 1," and savvy owners always look for ways to maximise this potential. In areas like Berwick and Narre Warren, parking ratios are a critical value driver for retail and office assets. If your building lacks adequate on-site parking, its appeal to high-quality medical or professional tenants diminishes rapidly. Consider the refurbishment potential as well; can the space be easily subdivided or repurposed? Modern office complexes also benefit from high NABERS energy ratings, which attract corporate tenants and satisfy the increasing demand for sustainable, high-performing workspaces. These tangible and intangible factors work in unison to define your asset's elite status in the Melbourne market.

Step-by-Step: How to Prepare for a Professional Commercial Appraisal

A professional appraisal is more than a simple walk-through; it's a high-stakes financial audit of your asset's performance. When considering how to value my commercial property, you must view the process through the eyes of a valuer who is trained to identify and quantify risk. A cluttered file or a neglected facade suggests mismanagement, which can subtly influence the risk premium applied to your yield. Preparation starts long before the valuer arrives on-site in the City of Casey.

The Essential Document Checklist

Organise your paperwork to present a "clean" investment case. Valuers rely on primary evidence. If your records are incomplete, they may use conservative market averages instead of your actual, potentially higher, figures. Ensure you have the following ready:

- Current lease agreements: Include all variations, side letters, and signed extensions to prove income security.

- Schedule of outgoings: Provide detailed receipts for council rates, water, insurance, and land tax.

- Compliance documents: Collate your annual fire safety statements and recent HVAC service records.

- Capital expenditure history: Compile a list of recent structural improvements or maintenance upgrades to justify a lower depreciation rate.

Maximising First Impressions

Your property's physical condition must reflect its premium status. First impressions often dictate the narrative of the entire appraisal. Ensure the facade and signage areas are pristine; clean the exterior and remove any outdated tenant branding or graffiti. Verify that all essential services, including lifts and fire systems, are recently serviced and fully compliant. Addressing minor repairs now prevents them from being flagged as "deferred maintenance," a term that can negatively impact your final figure.

Mastering how to value my commercial property also requires a deep dive into your net income. Scrutinise your outgoings to ensure every recoverable expense is accounted for. With the Reserve Bank of Australia holding the cash rate at 4.35% in May 2026, every dollar of net income is vital for maintaining your valuation in a high-interest environment. Look for "hidden" value drivers that a standard appraisal might miss. Do you have unused air rights or a current development permit for an extension? Highlighting these opportunities can shift your property from a standard asset to a high-potential investment. Ready to see where your asset stands in the current market? Request a free property appraisal from our local specialists today.

Strategic Valuation: Maximising Your Asset’s Potential in the South East

Maximising your asset's potential in the South East requires moving beyond generic spreadsheets and into the reality of the City of Casey's local economy. If you're still wondering how to value my commercial property using online calculators, you're likely missing the nuance of the industrial boom in Pakenham and Officer. Industrial vacancy in the South East hit a record low of 3.7% in late 2025, which continues to drive rents higher and compress yields for prime assets. This hyper-local demand creates a valuation environment where generic data simply won't suffice.

The transition from stamp duty to the annual Commercial and Industrial Property Tax (CIPT) is another structural shift that sophisticated investors must navigate. For properties entering this system, the 1% annual tax on unimproved land value becomes a critical factor in long-term holding costs. This makes the accuracy of your initial appraisal even more vital. Understanding how these legislative changes interact with the 4.35% cash rate allows you to position your asset as a high-performing financial instrument rather than just a physical building.

Local Market Dynamics in the City of Casey

Infrastructure projects in Pakenham are fundamentally reshaping commercial demand across the corridor. New transport links and industrial precincts are attracting national tenants who previously only looked at the inner suburbs. We're seeing a distinct "flight to quality" where modern, well-located offices in Berwick are outperforming older secondary stock. These prime assets attract lower yields because they offer long-term security and lower maintenance risks. Only deep local expertise can accurately distinguish between a 5.25% and a 6.00% Cap Rate based on street-level demand and specific precinct performance within the South East.

Partnering with Elite Agents & Partners

Our team provides a distinct advantage by using real-time leasing data from our commercial leasing and management portfolio to justify higher appraisals. We don't just look at what sold last year; we look at what tenants are signing for today. This sophisticated approach to lease negotiation helps build long-term asset value by securing high-quality covenants and favourable rent review structures. Our tailored marketing campaigns are designed to reach high-net-worth investors who value the transparency and professional authority we bring to every transaction. Moving from a DIY estimate to a professional market appraisal is the first step in unlocking your property's true worth. Take the next step in your investment journey and Request your complimentary commercial market appraisal today.

Unlocking Your Asset's True Market Potential

Mastering the intricacies of income capitalisation and the WALE factor is the hallmark of a sophisticated investor. You've seen how precise documentation and a clean net income profile can significantly compress your yield and boost your property's valuation. While understanding the theory of how to value my commercial property is a powerful first step, the final result depends on real-time data from the Berwick and City of Casey markets.

We specialise in navigating the unique dynamics of the South East, from expert lease negotiation for premium results to comprehensive management for sophisticated portfolios. Our team combines technical rigour with localised knowledge to ensure your asset is positioned at its absolute peak. Don't leave your equity to chance in a shifting interest rate environment. Take the next step toward securing your financial future and Book an Elite Commercial Appraisal for Your Property today. We look forward to partnering with you to achieve exceptional outcomes for your commercial investment.

Frequently Asked Questions

How is a commercial property valuation different from a residential one?

Commercial valuations are primarily driven by the income the asset generates rather than the emotional or lifestyle factors that influence residential sales. While a house is valued on comparable sales of similar homes, a commercial appraisal focuses on the net income, lease strength, and the prevailing market yield. It is essentially a financial assessment of a business-producing vehicle where the physical structure serves as the shell for cash flow.

What is a "good" capitalisation rate for a warehouse in Pakenham?

A "good" cap rate depends on the asset's quality and tenant profile, but current benchmarks for industrial stock in the South East range between 5.25% and 6.00%. Prime warehouses in Pakenham with modern facilities and long-term tenants often sit at the sharper end of this scale. If you are looking at how to value my commercial property in this precinct, remember that lower risk profiles command lower cap rates and higher total values.

Does a vacant commercial building have any value?

Yes, a vacant building retains significant value, though the valuation method usually shifts from Income Capitalisation to Direct Comparison. Instead of yield, the valuer looks at the rate per square metre achieved by similar vacant sales in the area. These properties often appeal to owner-occupiers who are willing to pay a premium to secure a permanent base for their own business operations rather than seeking a rental return.

How much does a professional commercial valuation cost in Victoria?

Professional fees for a formal valuation vary widely based on the asset's complexity, size, and the specific purpose of the report. A valuation for a small retail strip will differ in cost from a large-scale industrial complex or a multi-tenanted office tower. You should expect to pay a fee that reflects the professional liability and technical expertise provided by an API-certified valuer; however, many investors start with a market appraisal to gauge current sentiment.

Can I increase my property value by changing the lease terms?

You can significantly boost your asset's value by negotiating more favourable lease terms that reduce investor risk. Extending the lease expiry to increase the WALE or shifting from a gross lease to a net lease where the tenant pays outgoings directly improves the bottom line. These strategic adjustments make the income stream more attractive to buyers, which can lead to a compression of the cap rate and a higher overall valuation.

What is the difference between a bank valuation and a market appraisal?

A bank valuation is a conservative assessment designed to protect the lender's interests by identifying the "worst-case" recovery value. A market appraisal is a strategic estimate of what a motivated buyer or tenant is likely to pay in the current climate. Understanding how to value my commercial property through an appraisal gives you a realistic view of your equity and market position, which is often higher than a bank's cautious figure.

How often should I have my commercial property valued?

Most sophisticated investors review their property's value every 12 to 24 months to ensure their portfolio remains optimised. With the RBA cash rate sitting at 4.35% and the introduction of the Commercial and Industrial Property Tax (CIPT) reforms, market conditions are moving quickly. Regular valuations help you stay ahead of yield shifts, manage your insurance requirements accurately, and identify the right moment to refinance or divest.

Does the tenant’s business type affect my property’s value?

The tenant's business type and financial "covenant" are critical factors that directly influence the risk profile of your investment. A national brand or an essential service provider like a medical clinic is viewed as a lower risk than a niche start-up or a hospitality venture. Lower risk allows valuers to apply a sharper cap rate, which increases the capital value of your property because the income is perceived as more secure.